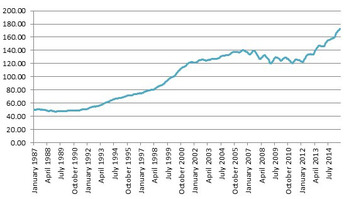

Case-Shiller: Denver Ties for 1st Place10/28/2015  Homes in the Denver skyrocketed by 10.7 percent in August, tying the metro area with San Francisco for the No. 1 spot on the closely watched Case-Shiller index released today.

The year-over-year percentage gain ties a record Denver set in August 2001, according to the S&P/Case-Shiller Price Indices, which tracks home sales in 20 major metropolitan statistical areas. The last time Denver homes rose by 10.7 percent, the average 30-year, fixed-rate mortgage was 6.95 percent, compared with 3.91 percent in August of this year and the inflation rate in August 2001 was 2.72 percent, more than 10 times higher than the inflation rate of 0.2 percent in August. August also marked the 42nd consecutive month that home prices in the Denver area have set a record, according to Case-Shiller. However, given the housing appreciation, tracked by Case-Shiller and other groups including the Denver Metro Association of Realtors, the Colorado Association of Realtors and Zillow, affordability is a big issue, especially for first-time home buyers. “When the construction defect issues are resolved, we will start seeing more entry-level condos being built, instead of all of these apartment buildings,” Bauer said. Anthony Rael, chairman of the DMAR Trends Committee and a broker with RE/MAX Alliance, agrees. “We’ve been worried about housing affordability every month for the past 18 months,” Rael said. “Every mayor in the country, and especially mayors in Denver and the surrounding areas, are especially worried about housing affordability,” he said. It is increasingly tough for builders to bring entry-level homes to the market, he said. “With rising labor costs, rising land costs and still high material costs, the economics are such that it is really hard to build affordable houses,” Rael said. “I don’t know what the answer is,” especially since it is hard to convince politicians and taxpayers that affordable housing needs to be subsidized, he said. He is increasingly seeing sellers with homes in the $500,000-plus range dropping the asking price by as much as $30,000. “I think these sellers missed the market,” and find they can’t match the frenzy of last summer, he said. “But starting in late February, unless we see a plethora of new listings dumped on the market, which I don’t expect, I think we are going to start this cycle all over again,” Rael said. “Hopefully, it won’t be quite so frenzied; I think last summer was unprecedented. I hope it is. It would be pretty scary if we had another summer like that, as the kind of price appreciation we saw last summer is not sustainable and not healthy for the overall market and the economy.” Still, Rael was not surprised by the 10.7 percent gain in the Case-Shiller report. “It is pretty consistent with that the Denver Metro Association of Realtors, the Colorado Association of Realtors and others reported,” Rael said. On a national front, there is a lot of good housing news to report. “Home prices continue to climb at a 4 percent to 5 percent annual rate across the country,” said David M. Blitzer, Managing Director and Chairman of the Index Committee for S&P Dow Jones Indices. “Most other recent housing indicators also show strength,” Blitzer continued. “Housing starts topped an annual rate of 1.2 million units in the latest report with continuing strength in both single family homes and apartments,” Blitzer said. “The National Association of Home Builders sentiment survey, reflecting current strength, reached the highest level since 2005, before the housing collapse. Sales of existing homes are running about 5.5 million units annually with inventories of about five months of sales,” he said. However, September new home sales took an unexpected and sharp drop as low inventories were cited as a possible cause. “A notable part of today’s economy is the continuing low inflation rate; in the year to September, consumer prices were unchanged,” Blitzer said. “Even excluding food and energy, the core inflation was 1.9 percent. One result is that a 5 percent price increase in the value of a house means more today than it did in 2005-2006, the peak of the housing boom when the inflation rate was higher,” Blitzer explained. “The rebound from the recent lows was faster than the 1997-2005 housing boom, and also much less driven by inflation,” he concluded. Mortgage Blog – October 26, 201510/26/2015  Last week’s economic news included the National Association of Home Builders Index, Housing Starts and FHFA’s report on August home sales. The National Association of Realtors® released its monthly report on sales of previously owned homes.

Builder Confidence and Housing Starts Post Gains The Wells Fargo National Association of Home Builders Housing Market Index for September posted its highest level of builder confidence in 10 years a higher than expected results with a reading of 64 for October. Analysts expected a reading of 62 based on September’s reading of 61. The NAHB Wells Fargo Housing Market Index reading is based on three builder confidence readings. Builder confidence in current market conditions rose three points to a reading of 70; builder confidence in housing market conditions over the next six months rose seven points to 75 and buyer traffic in new housing developments held steady with a reading of 47. Any reading over 50 indicates that more builders are confident about market conditions than those who are not. This news was consistent with September housing starts, which were also higher. The U.S. Commerce Department reported September’s housing starts at an annual level of 1.206 million starts against expectations of 1.139 million starts and August’s reading of 1.132 million housing starts. Sales of Previously Owned Homes Surpass Expectations September sales of pre-owned homes surpassed expectations according to a report released by the National Association of Realtors®. Sales of previously owned homes reached 5.55 million sales on a seasonally-adjusted annual basis against an expected reading of 5.34 million sales. August’s reading was adjusted downward from 5.31 million sales to 5.30 million sales of previously owned homes. Lawrence Yun, Chief Economist for the National Association of Realtors®, cited lower mortgage rates, higher demand for homes and low inventories of available homes as driving higher sales. Slight easing of mortgage credit standards was also said to be driving home sales. FHFA’s Home Price Index for August showed that home prices for properties associated with mortgages owned by Fannie Mae and Freddie Mac increased at a rate of 5.05 percent in August as compared to a growth rate of 5.80 percent year-over-year in August 2014. Mortgage Rates Mixed, Weekly Jobless Claims Lower Weekly reports on mortgage rates and jobless claims yielded mixed results. Freddie Mac reported that average rates for fixed rate mortgages dipped with the average rate for a 30-year fixed rate mortgage three basis points lower at 3.79 percent; the average rate for a 15-year fixed rate mortgage fell by five basis points to 2.98 percent. The average rate for a 5/1 adjustable rate mortgage ticked upward by one basis point to 2.89 percent. Average discount points were 0.60 percent for a 30-year fixed rate mortgage, 0.50 percent for a a5-year fixed rate mortgage and were unchanged at 0.40 percent for a 5/1 adjustable rate mortgage. Weekly jobless claims were lower than expectations with a reading of 259,000 new claims filed against expectations of 265,000 new jobless claims. New claims were higher than the previous week’s reading of 256,000 new claims. Analysts are keeping an eye on jobs reports as stronger job markets are essential to expanding home sales. What’s Ahead This week’s scheduled economic news includes Case-Shiller reports on home prices along with reports on new home sales, consumer confidence and consumer sentiment. Core inflation readings will be released Friday after Thursday’s releases of Freddie Mac mortgage rates and weekly jobless claims.  This is not available for all types of purchase loans, and will be flagged as “inducement to buy” if a seller tried to help a buyer purchase their home, with no existing relationship with them.

For families however, this creates a perfect opportunity for a family member to purchase the home, using the equity in the home, as their down payment. This works well in situations where aging parents are wanting to down size and cash out to enjoy their golden years. They are finally relieved of their mortgage if any, and are giving their kids the gift of home ownership, letting them keep the home in the family. The following 2 examples are of 2 gift of equity purchases that are both different in nature, however provide the same result for the buyer, one with just a larger down payment. Example #1 John and Julie currently rent a home, which their mom currently owns free and clear. They want to purchase the home from her, so she can cash out of her home, and enjoy her retirement. The sales price their mom has agreed to is $250,000. She has agreed to pay $5000 in closing costs, and Equity Gift he daughter the minimum FHA down payment of 3.5%, which equates to $8,750, totaling $13,750. At closing Julie’s mom will receive a proceed check for the $250,000 minus the $13,750 in gift of equity and closing costs. Example #2 Owen wants to buy his Dad’s house however does not currently live there. The home is free and clear and Owen’s Dad has agreed to the purchase. The sales price is $300,00, however since Owen does not live there, the minimum down payment is 15%. Owens Dad has agreed to pay closing costs of $5000. At closing, Owens Dad will receive a proceed check of $250,000 which is taking out the 15% down payment of $45,000 and closing costs of $5000. In closing the gift of equity works in certain unique situations, and cannot be used for any buyer to purchase from any seller, as that creates collusion of funds, and is considered an inducement to buy. The gift of equity purchase cannot be used to save a family member from foreclosure if they are behind on the mortgage, and should only be used in the examples I have provided above, or ones similar in nature. Call me with any questions you might have 303.668.3350!  It’s difficult to begin shopping around for a new mortgage without the facts on how this can affect your FICO score.Anybody who is holding off for fear that their credit score will be ruined by multiple credit checks has nothing to worry about. Mortgage brokers require this information to give an accurate quote, so many credit checks by different companies will have a minuscule effect on credit scores.

The system has been designed this way because a mortgage is not considered to be ‘bad debt’ by lenders and consumers should have the right to shop around without fear of their credit being destroyed by it. Understanding The ‘Tiers’ Of Credit Checks FICO scores are affected each time a credit inquiry is requested to check a borrower’s credit report. This makes sense, as every time somebody searches for new credit they increase their ability to acquire significant debt. Thankfully, not all credit checks are created equal and they do not affect FICO scores in the same way. A mortgage loan is not considered remotely close to store credit cards, which allow a person to get into more debt. Debts on mortgages only get lower as time goes on, ranking them very low on the list of things lenders consider bad credit. The One Thing To Know Before Shopping For A New Mortgage Every time a credit card company or consumer loan company pulls a credit check, the borrower’s FICO score will fall, but this will not happen when multiple mortgage lenders pull the same person’s credit score. This is because each credit card has the chance to accumulate debt, whereas only one mortgage will be taken out. So once a mortgage lender pulls your credit score, you will only receive one ‘ding’ even if other lenders pull your score afterwards. Here is the important part: there is only a 14 day window from the first credit check where all other credit inquiries will be ignored. So it is imperative to plan ahead and shop around within a two week period to limit the impact on your FICO score. Shopping around when looking for a new mortgage is a necessary step to getting the best possible deal, and thankfully the system is designed around not punishing people for doing this. It can be very intimidating to do alone and working with a professional mortgage specialist can relieve stress and get you the best deal on your new mortgage. If you have any questions please contact me direct at 303.668.3350 for advice on the right steps to getting your new mortgage.  Whether you’re planning on selling your home soon or you want to do a few minor renovations for your own enjoyment, an ailing hardwood floor may be on your list of things to tackle.

While this can be a more difficult renovation to complete than many other household items, here are five reasons you may want to move it to the top of the list. An Issue with Structure If there happens to be any glaring structural issues with your hardwood, a complete do-over will be a necessity if you want to sell your house in the future. While this will likely involve fixing the sub-floor under your hardwood, this will dramatically improve the overall health of your home. Experiencing a Lot of Movement? A lot of movement in your hardwood floor can be a sign that it’s time for a fix up. If you’re already planning on refinishing your floor for an instantly improved look, this fix-up will need to happen before you can take that necessary next step! Worn-Out or Over-Sanded Wood Whether your boards are worn down in spots from excessive use or sanding, this is an issue that will instantly age the look of your living space. If you’re noticing the boards coming apart at the ends or nails jutting out, it’s definitely time for an overhaul. Upping a Home’s Market Value There may be a few things a home buyer will be willing to fix in a new home, but flooring is unlikely to be something they will want to replace right off the bat. By upgrading this before it’s an issue, you can easily make your home a lot more attractive to potential buyers and increase the value of your home. It’s an Instant Face lift There are few things that will be as apparent as the look of the floor when entering a room, so having dull, scratched hardwood will instantly downgrade the appearance of your living space. If more than expected wear and tear has occurred, an updated floor can completely shift the look of your place! If you’re planning on improving your home and tackling a home renovation soon and are not sure where to begin, you may want to assess the quality of life left in your flooring. As this will have a marked impact on the way your home appears, fixing your floors can help to improve the market value of your home. If you’re wondering about other renovation upgrades consider contacting me direct at 303.668.3350 for more information about what will add the most value to your investment.  If not done properly, applying for a mortgage can be stressful and time consuming, but with the right preparation the entire process can be seamless. Here are some crucial pieces of information that almost any lender will require before approving a mortgage.

Tax Information From The Previous Two Years One of the most important documents a borrower will be asked for is their federal tax return along with a signed Form 4506-T, which will allow the lender to contact the IRS directly for their version of the federal tax return to compare to the ones provided. This allows them to examine the documents for any sign of fraud. Documentation On All Owned Assets The mortgage lender will require proof of every current asset owned by the borrower. This will include any current real estate titles along with bank and mutual fund statements and documentation on current investments. Don’t be shy, every asset owned is a better sign to the lender. Documentation On All Owed Debts On the opposite side of the coin, the mortgage lender will also want to be made aware of any current debt. All debts, from major student loans to minuscule credit card debts, will need to be documented and given to the lender. It’s important to provide information on monthly payments that need to be made, even if it appears insignificant. Two Years Of W-2s For Employed Borrowers Almost every lender will require a Form W-2 for the previous business year to see how much income was earned by the borrower. Many will require at least two years’ worth of W-2s to see if the income has been consistent. Two Years Of 1099s For Self-Employed Borrowers Alternatively, any self-employed borrowers will be required to provide profit and loss statements to show the current status of their business. Like W-2s, the lender may require documents showing profit and losses for at least two years if the business has been in existence that long. Having all your documents ready in advance to applying for a mortgage can go a long way to helping the process go smoothly. The documents needed for a mortgage change from person to person depending on their situation, so make sure you speak with a qualified mortgage professional in advance to get a better idea of which documents you will need to supply.

Archives

February 2023

Categories |

RSS Feed

RSS Feed

Popular Pages |

Company

|

Equal Housing Lender licensed through NMLS Regulated by the Division of Real Estate. Licensed Mortgage Loan Originator licensed in Colorado and California. Not endorsed or sponsored by either state or any government agencies.